How to Balance Travel Goals with Other Financial Priorities

Did you know that 73% of Americans say they want to travel more, but only 34% actually prioritize it in their budget? If you’ve ever felt torn between booking that dream vacation and paying off debt, saving for a house, or building your emergency fund, you’re not alone. I’ve been there too—staring at flight deals while my student loan balance glared back at me from another browser tab. Learn how to balance travel goals with financial priorities.

The good news? You don’t have to choose between living your life and being financially responsible. With the right strategies and mindset, you can pursue your travel goals while still making progress on other important financial priorities. Let me show you exactly how to create a balanced approach that works for your unique situation.

You may also like this:

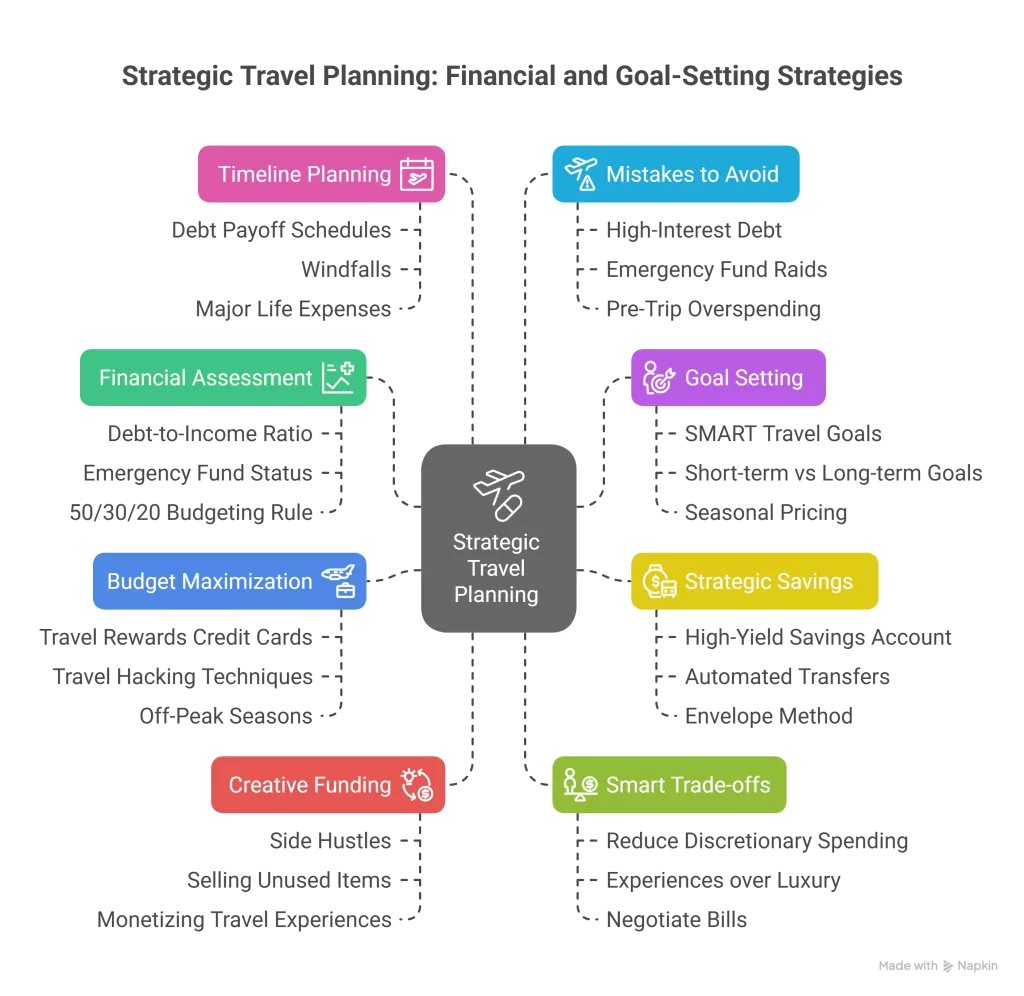

Assess Your Current Financial Landscape Before Planning Travel

Before you start dreaming about balancing travel goals with other financial priorities, you need a crystal-clear picture of where your money actually goes each month. Start by listing all your income sources and fixed expenses—rent, utilities, minimum debt payments, and insurance. According to financial experts, your debt-to-income ratio should be below 36% to maintain healthy finances while pursuing travel goals.

Next, examine your emergency fund status. Financial advisors recommend having 3-6 months of expenses saved before allocating significant funds to travel. This doesn’t mean you can’t travel at all, but it helps you determine how aggressively you can pursue your wanderlust. Use the 50/30/20 budgeting rule as your foundation: 50% for needs, 30% for wants (including travel), and 20% for savings and debt repayment. Within that 30% “wants” category, decide what percentage feels realistic for travel without compromising your other financial goals.

Set SMART Travel Goals That Align with Your Financial Reality

Vague travel dreams like “I want to see Europe” won’t help you balance travel goals with other financial priorities effectively. Instead, create SMART travel goals that are Specific, Measurable, Achievable, Relevant, and Time-bound. For example: “Save $3,000 for a 10-day Italy trip by September 2025.”

Break your travel aspirations into short-term goals (trips within 12 months) and long-term goals (18+ months away). Short-term goals might include weekend getaways or domestic trips costing $500-2,000, while long-term goals could involve international adventures requiring $3,000-8,000. Consider seasonal pricing fluctuations—traveling to Europe in shoulder season can save you 30-40% compared to peak summer rates.

Prioritize your travel experiences based on personal values. Are you seeking adventure, relaxation, cultural immersion, or family time? This helps you allocate your travel budget more intentionally and ensures each trip aligns with what truly matters to you while maintaining progress on your other financial priorities.

Create a Strategic Travel Savings Plan Alongside Other Priorities

The secret to successfully balancing travel goals with other financial priorities lies in treating your travel fund like any other essential expense. Open a dedicated high-yield savings account specifically for travel—this psychological separation makes it harder to “borrow” from your vacation fund for everyday expenses. Online banks like Ally or Marcus typically offer rates 10-15 times higher than traditional savings accounts.

Automate your savings transfers immediately after each paycheck. If you’re saving for both travel and an emergency fund, consider splitting your savings goal—perhaps $200 monthly to emergency savings and $150 to travel. The “pay yourself first” principle ensures your financial goals get funded before discretionary spending takes over. Use the envelope method by creating separate digital or physical envelopes for each goal: emergency fund, travel, retirement, and debt payoff.

Calculate exactly how much you need monthly to reach each goal. For a $3,000 trip in 12 months, you’ll need to save $250 monthly. Break this down further—that’s roughly $58 per week or $8.25 daily. When you see these smaller numbers, your travel dreams suddenly feel much more achievable alongside your other priorities.

Maximize Your Travel Budget Through Smart Money Strategies

Smart travelers know that maximizing your travel budget isn’t about spending less—it’s about spending strategically. Travel rewards credit cards can be game-changers when used responsibly. Cards like the Chase Sapphire Preferred or Capital One Venture can earn you 40,000-60,000 bonus points (worth $400-800 in travel) after meeting spending requirements. However, only use these cards if you can pay the full balance monthly; interest charges will quickly erase any rewards benefits.

Master basic travel hacking techniques to stretch your dollars further. Sign up for airline newsletters to catch flash sales, use fare comparison tools like Google Flights or Skyscanner, and set up price alerts for your desired routes. Shoulder season travel can save you 30-50% on flights and accommodations—visit Europe in late spring or early fall instead of peak summer.

Consider alternative accommodations that align with your goal to balance travel goals with other financial priorities. Vacation rentals often cost less than hotels for longer stays, while house-sitting can provide free accommodation in exchange for pet care. These strategies help you travel more frequently without derailing your other financial commitments, proving that smart planning beats a big budget every time.

Find Creative Ways to Fund Your Travel Without Compromising Other Goals

When traditional budgeting isn’t enough to balance travel goals with other financial priorities, it’s time to get creative with income generation. Side hustles can be your travel fund’s best friend—freelance writing, tutoring, or driving for rideshare services can easily generate an extra $200-500 monthly. The beauty of side hustle income is that it doesn’t compete with your regular budget allocations for essentials or other financial goals.

Start by selling unused items around your home. That exercise equipment gathering dust or designer clothes you never wear could fund a weekend getaway. According to decluttering experts, the average household has $3,000 worth of unused items—more than enough for a solid vacation fund boost.

Consider monetizing your travel experiences themselves. Travel blogging, Instagram partnerships, or creating travel guides can generate income while you explore. Even small accounts can earn $100-300 per sponsored post. Remote work opportunities are also expanding rapidly—negotiate with your employer for occasional work-from-anywhere days, or transition to a fully remote role that allows location independence. These strategies help you fund travel dreams without touching your emergency fund or derailing debt payoff plans.

Make Strategic Trade-offs That Don’t Sacrifice Long-term Security

Successfully balancing travel goals with other financial priorities often requires making intentional trade-offs that align with your values. The key is choosing temporary spending reductions rather than permanent lifestyle downgrades. Analyze your discretionary spending for the past three months—you might discover you’re spending $150 monthly on dining out or $80 on subscription services you rarely use.

Consider the opportunity cost of luxury purchases versus travel experiences. That $1,200 designer handbag could fund a week in Costa Rica, while skipping your daily $5 coffee habit saves $1,800 annually—enough for multiple domestic trips. Delay non-essential major purchases like furniture upgrades or the latest tech gadgets for 6-12 months while you build your travel fund.

Get strategic about entertainment costs at home. Host potluck dinners instead of expensive restaurant nights, explore free local events, or have movie nights at home rather than theater visits. Negotiate your bills regularly—call your phone, internet, and insurance providers to request better rates. Many people save $50-100 monthly just by asking. These small sacrifices create significant travel funding without compromising your emergency savings, retirement contributions, or debt repayment progress. Remember, these trade-offs are temporary investments in the experiences that matter most to you.

Plan Your Travel Timeline Around Major Life Financial Milestones

Smart timing can make the difference between struggling to balance travel goals with other financial priorities and achieving both seamlessly. Coordinate your travel timeline with major financial milestones to maximize opportunities and minimize stress. If you’re following a debt snowball or avalanche method, plan smaller trips during the payoff period and save your dream destinations for after you’re debt-free—the psychological reward will be even sweeter.

Strategic timing around windfalls can supercharge your travel fund without derailing other goals. Tax refunds, work bonuses, or side hustle income spikes provide perfect opportunities for travel funding. The average American receives a $2,800 tax refund—enough for a significant domestic trip or solid foundation for international travel savings.

Consider your life stage and upcoming major expenses. If you’re planning to buy a house in two years, prioritize travel experiences now while your housing costs are predictable. Wedding planning? Take that honeymoon-preview trip before the big expenses hit. As your income grows throughout your career, implement graduated travel experiences—start with regional adventures in your twenties, upgrade to international trips in your thirties, and plan luxury experiences as your earning power peaks. This approach ensures you’re always traveling within your means while building toward bigger adventures.

Avoid Common Financial Mistakes That Derail Travel Dreams

The fastest way to sabotage your ability to balance travel goals with other financial priorities is falling into common financial traps that seem harmless but create long-term damage. Never finance travel with high-interest debt—that $3,000 European adventure becomes a $4,500+ burden when put on a credit card with 22% APR and minimum payments. If you can’t pay cash for the trip, you’re not ready to take it yet.

Your emergency fund is not a travel fund, no matter how tempting it becomes when you see flight deals. Emergency funds exist for genuine emergencies—job loss, medical expenses, or major home repairs. Raiding this safety net for vacation leaves you financially vulnerable and defeats the purpose of building financial security alongside travel experiences.

Pre-trip overspending is another budget killer. You don’t need $500 worth of new luggage and travel gear for every trip. Resist the urge to completely overhaul your wardrobe or buy every travel gadget that influencers recommend. Similarly, don’t sacrifice retirement contributions for short-term travel gains—compound interest can’t be recovered later. Finally, budget for the complete trip cost, including airport parking, meals, activities, and souvenirs. Many travelers budget only for flights and hotels, then return home with credit card debt from unexpected expenses. Plan for 20-30% more than your initial estimates to avoid financial stress during and after your adventures.

Conclusion

Balancing travel goals with other financial priorities isn’t about perfect math—it’s about intentional choices that align with your values. Remember, the best financial plan is one you can actually stick to, and that includes making room for the experiences that bring you joy.

Start small, be consistent, and celebrate your progress along the way. Whether you’re saving for a weekend getaway or a month-long adventure, every dollar saved is a step closer to your travel dreams and financial security.